Topic: Insurance

Leaving Manitoba

Collector Qualification Form

Customer Authorization

Snowmobiles

Rental Vehicle Insurance

New Vehicle Protection

Motorcycles

Loss of Use

Leased Vehicle Protection

Lay-up

Deductibles

All-Terrain Vehicles and other Off-Road Vehicles

The Collector Vehicle Program (CVP) is an option designed to meet the needs of Manitobans who own eligible collector vehicles. The program provides superior year-round insurance coverage and reflects the infrequent use of collector vehicles and the extraordinary care and maintenance owners provide for them.

To be eligible for the CVP, a vehicle must be:

- a passenger vehicle, light truck (gross vehicle weight of 4,540 kgs or less) or motorcycle, which has a valid safety Certificate of Inspection to confirm it meets, at time of inspection, basic standards for operation in Manitoba. Read more details here.

- used for ‘Pleasure’ only under Basic Autopac (i.e., not used for regular commuting)

- at least 25 years old

- maintained at a value of at least $5,000 for passenger vehicles and light trucks or over $4,000 for motorcycles

The program offers Basic all-perils insurance protection throughout the year, with the convenience of not having to switch to Lay-Up or another insurance product in the winter months. Basic Autopac provides more comprehensive coverage and greater protection than Lay-Up coverage.

All customers who participate in the CVP will obtain a unique collector licence plate.

Because motorcycles already benefit from this kind of year-round insurance coverage, motorcycle owners participating in the CVP will not see any change to their insurance coverage or premiums.

Is it right for me?

There are a variety of benefits to insuring your vehicle with the CVP, including:

- Basic Autopac coverage, including $750 deductible, $500,000 third-party liability and $70,000 maximum insured value

- Options to lower your deductible ($500, $300, $200 Standard and $200 Plus)

- Options to increase your third-party liability ($1 million, $2 million, $5 million, $7 million or $10 million)

- Excess Value coverage options for high-value vehicles

- Loss of Use options

As part of your enrolment, Basic Autopac and any purchased insurance options are provided year-round. That means there’s never any need to switch to Lay-Up coverage in the winter months, resulting in fewer trips to your Autopac agent’s office. Vehicle registration will also be provided year-round and registration charges will not be seasonally rated – enabling you to take your vehicle for a spin regardless of the season.

With the CVP, owners of eligible cars and light trucks can choose how their insurance works. In some cases, purchasing a combination of Lay-Up and Basic Autopac may result in less expensive premiums, although Lay-Up does not provide all-perils coverage. For example, the following chart shows the various options available for a 1969 Ford Shelby Mustang GT350*, using non-current premium cost examples for illustration purposes:

|

Insurance Type |

Insurance Premium Cost Example* |

Visits to Agent |

Distinctive Collector Plate |

Year-Round Road Coverage |

Year-Round Third Party Liability |

|

Collector Use – |

$283 |

One |

Yes |

Yes |

Yes |

|

Pleasure Use – |

$651 |

One |

No |

Yes |

Yes |

|

Pleasure Use – |

$351 |

Multiple |

No |

No |

No |

* Premium examples are not current and are for illustration purposes only. Does not include registration fees, plate fee or short-rate cancellation fees that may be applicable.

How do I join the CVP?

Please read and follow these instructions carefully or your entry into the CVP may be delayed:

Step 1) Qualify your vehicle

Fill out the Collector Vehicle Qualification Form (for passenger vehicles and/or light trucks only) and contact a Manitoba Association of Automobile Clubs (MAAC) CVP qualifier directly to arrange an appointment to present your vehicle.

(Note: If you are the owner of a motorcycle, you are not required to fill out the Collector Vehicle Qualification Form. Please proceed directly to Step 2, where you will simply self-declare its value.)

MAAC, with its broad base of support from the collector vehicle owner community and the wide-reaching network of car clubs under its umbrella, is ideally suited to assist Manitoba Public Insurance with ensuring that vehicles meet the program criteria.

You may also choose to qualify your vehicle through Manitoba Public Insurance. To schedule an appointment, please call us at 204-985-7000 or toll free at 1-800-665-2410.

Step 2) Purchase your insurance and receive your CVP plate

You must visit your local Autopac agent or Service Centre to join the Collector Vehicle Program. This step cannot be done via email, standard mail or fax. Remember to bring your approved Collector Vehicle Qualification Form (passenger vehicles and light trucks).

Once you have submitted your form in person, your Autopac agent or a MPI Service Centre representative will provide you with your new collector plate.

Cancelling your CVP policy

You may cancel a CVP policy during the riding season and receive a refund for any unused portion. Please also note that if you choose to leave the CVP, you will be able to retain your CVP licence plate. However, you may have to re-qualify your vehicle should you later decide to re-join the program.

If you intend to give a collector licence plate as a gift, the registered owner must be part of the CVP with the designated vehicle.

Appeal process

If you disagree with a decision made by MAAC or Manitoba Public Insurance relating to eligibility for the CVP, you can file an appeal and provide your substantiated information by writing to:

Manitoba Public Insurance

Registrar of Motor Vehicles

c/o Collector Vehicle Program Appeal

PO Box 6300

Winnipeg, MB

R3C 4A4

If you need to rent or borrow a vehicle, it’s a good idea to think about the insurance protection you’ll need. Rental Vehicle Insurance from Manitoba Public Insurance provides better coverage at a substantially lower cost than most rental companies.

Renting can be risky

There’s more to renting a vehicle than you might think. Driving an unfamiliar vehicle in a strange place can make a collision more likely. Without the right insurance, you could wind up paying for damages and injuries from your own pocket. The financial risks of renting outside Manitoba are significant:

- First, others involved in a collision may claim against you. You could wind up with a huge bill for injuries to others and for damage to their property.

- Second, you’re personally responsible for damage to the vehicle you rent, whether or not you’re at fault. Most rental companies also charge “down-time” to compensate them for the time the vehicle is off the road being fixed or replaced.

- Finally, if your first rental vehicle is out of action because of a collision, you may need to rent another one at your own cost.

Coverage details

- Covers rented or borrowed private passenger vehicles, light trucks, motorcycles and mopeds in Canada or the United States.

- Up to $10 million for claims others may make against you.

- Up to $100,000 for damage to vehicles rented outside Manitoba.

- Daily allowances payable to you to rent a replacement vehicle and to cover “down-time” charges assessed to you by the rental company (subject to daily limits).

- Cost is based on where you rent, but you’re covered anywhere you drive in Canada or the United States – check with the rental company before taking their vehicle outside the province or state where you’ve rented it.

- Coverage periods from three to 90 days are available.

- $200 deductible (the amount you pay) on damage to the rental vehicle.

- Fast, friendly and familiar Autopac claim service should you become involved in a collision.

As a Manitoban you are covered by the Personal Injury Protection Plan (PIPP) if you are hurt in a collision while driving the rental vehicle.

Save money

Save up to $25 each day with Rental Vehicle Insurance compared to coverage from the rental company. The rate for Rental Vehicle Insurance is based on where the vehicle is rented, not where it is driven and you can drive the vehicle anywhere in Canada or the United States. For example, a customer who rents a vehicle in Winnipeg to drive to California pays the Manitoba rate, not the United States rate.

Manitoba rate – $3 per day

Canada rate – $6 per day

United States rate – $8 per day

A $15 policy fee and a minimum of three days of premium apply to each Rental Vehicle Insurance policy. Check our Rate Calculator for an estimate.

Who can buy

Rental Vehicle Insurance is only available to permanent or temporary Manitoba residents with a valid driver’s licence.

- Applicants must be at least 16 years of age.

- Any applicant under the age of 18 years must have a parent or legal guardian co-sign the application form.

- The Rental Vehicle Insurance policy and the rental agreement must both be in the name of the same person.

Who’s covered

Rental Vehicle Insurance covers you (the policyholder) and any other driver, provided the driver has your permission to drive the vehicle and is qualified or authorized by law to operate the vehicle. If the operator is not a Manitoba resident, they must be qualified or authorized by law in the jurisdiction where they reside.

With our Rental Vehicle Insurance, you don’t have to list all of your drivers. If you’ve bought our Rental Vehicle Insurance in your name, anyone driving the vehicle with your consent and with a valid driver’s licence is covered. However, the rental company may require you to list all your other drivers as part of their rental agreement.

Rules

- Rental Vehicle Insurance covers rented or borrowed cars, light trucks, passenger vans, motorcycles, mopeds and SUVs. A valid motorcycle licence is required to operate a motorcycle. Rental Vehicle Insurance doesn’t provide coverage for rented off-road vehicles, trailers, motorhomes, heavy trucks or buses.

- You must not use the rental vehicle for business deliveries.

- If you’ve bought Rental Vehicle Insurance under your name, make sure you rent the vehicle under your name too.

- If you need to keep your rental vehicle longer than planned, you cannot extend your RVI policy and will need to buy a new policy. You can make arrangements with your broker over the phone and they will fax you a copy of the new policy. The new policy must be concurrent to the first one, and payment must be made immediately by Visa or MasterCard.

- If you need to make a claim for damage on a vehicle you’ve rented, do so in the same way you would if you are involved in a collision with your own vehicle. Contact us to report your claim. Have your rental agreement and rental vehicle insurance policy on-hand when you call.

- Make sure you tell the rental company you have made a claim and that you have Rental Vehicle Insurance. If they do bill you, send the bill to the adjuster handling your claim.

For rentals in Manitoba

When renting or borrowing a vehicle that’s registered and insured in Manitoba, that vehicle’s Basic Autopac insurance covers you if you have a valid driver’s licence and you’re driving with the rental company or vehicle owner’s permission.

For this reason, you’re only responsible for the Basic deductible, which is $750 for policies with an effective date of April 1, 2021, or later. Buying Rental Vehicle Insurance lowers your deductible to $200.

Rental companies can claim against you for lost revenue if their vehicle is damaged and unavailable for rental. You could also face claims from others whose property you’ve damaged or for injuries you’ve caused that exceed the liability insurance on the rental vehicle. Rental Vehicle Insurance protects you against these financial risks too.

Other coverage options

Rental Vehicle Insurance from Manitoba Public Insurance is your best choice, but other options are available:

- Rental Company Collision Damage Waivers (CDWs) or Loss Damage Waivers (LDWs): The cost is usually higher than Rental Vehicle Insurance.

- Credit card coverage: Some credit cards automatically cover rental vehicles. Check with your credit card company to confirm if you have coverage and how it works. Coverage is usually less comprehensive than Rental Vehicle Insurance and specific restrictions normally apply.

- Your own Autopac coverage: A $1 million, $2 million, $5 million, $7 million or $10 million third-party liability coverage option transfers to a rented or borrowed vehicle. Transfer of third-party liability coverage to another vehicle is only effective for 30 days. This coverage doesn’t protect you against claims from the rental company for damage to their rental vehicle or for down-time. In the United States, it may not protect you fully against claims from other motorists. Therefore, it’s best not to rely on this coverage when renting or borrowing a vehicle in the United States.

If you need more information on Rental Vehicle Insurance, an Autopac agent will be happy to help you.

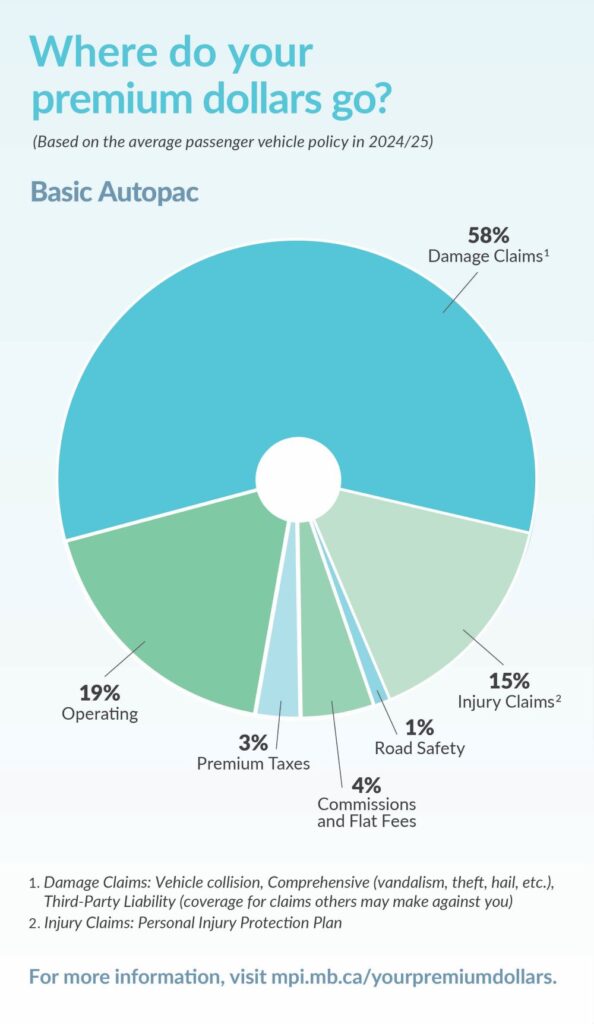

We believe in doing what’s right – which includes being open and transparent with you about what you are paying for when you insure your vehicle.

More information for customers

To be more accountable to you, we have introduced graphics on the front of our annual statements of account and renewal notices that feature a full breakdown of where your premium dollars go for both Basic and Optional Autopac, based on an average passenger vehicle policy.

Below is the information customers will receive:

You can find more details about this graphic below. Please note that all figures are rounded to the nearest one per cent for ease of reading.

Basic Autopac

There are three areas your Basic Autopac insurance premiums contribute to: damage claims, injury claims and expenses.

Damage claims

Damage claims pay costs to customers arising from collision, comprehensive (vandalism, theft, hail, etc.), and third-party liability claims (coverage for claims others may make against you).

Injury claims

The injury claims section represents payments related to Personal Injury Protection Plan (PIPP) claims. PIPP guarantees that any Manitoban injured in an automobile collision anywhere in Canada or the U.S. receives comprehensive and world-class injury and economic loss coverage. Learn more.

Expenses

Running a business, including public auto insurance, includes expenses. To ensure that we are able to continue to deliver exceptional coverage and service, affordable rates and safer roads to you, our expenses include:

Operating expenses: This includes all of the expenses related to processing your claims. It also covers all non-claims related expenses, such as employee compensation, regulatory, and reinsurance costs. Note that operating expenses are net of any services fees collected (such as late payment fees, financing fees, etc.)

Commissions: Brokers receive a commission from MPI when performing transactions on MPI products and services.

Premium taxes: A three per cent provincial tax is charged on all premiums.

Road safety: As a key part of our mission, we are committed to increasing public awareness about risky driving behaviours and to providing more opportunities for Manitobans to enhance their driving skills. We do this through supporting community-based programming with our stakeholders and partners that promotes road safety awareness and education, developing and managing awareness and education initiatives as well as conducting research and analysis to better understand road safety issues. Learn more.

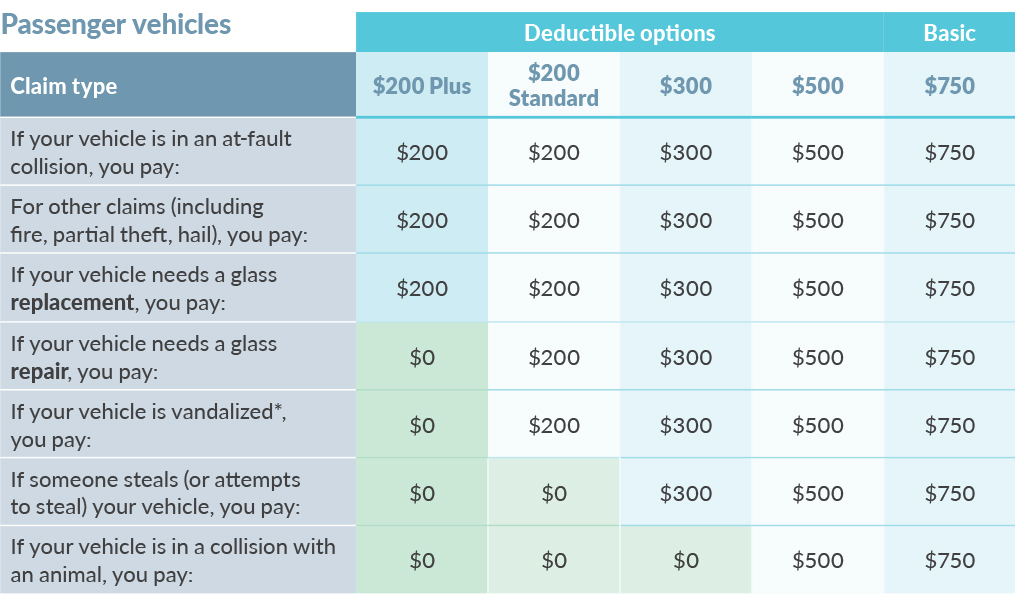

Know your options?

We’ve made improvements to deductibles, Third Party Liability and Max Insured Value coverages.

Your deductible

The deductible is the amount you pay as part of an Autopac claim. Your insurance covers the rest.

Your deductible applies to:

Personalized protection

Choose coverage and payment options that best suit you.

The basic deductible for private passenger vehicles is $750. A $750 deductible means you pay less for your annual insurance. For those drivers with a low incident risk, saving more on insurance might be a higher priority.

For drivers wanting minimum expense in the case of an Autopac claim, lower deductible levels of $500, $300 and $200 Standard or $200 Plus are available. (Yes, there is now two $200 deductible options!)

Know your options. See the comparison chart below to see what you would pay per claim type based on your deductible option.

For more information, visit your Autopac agent today.

One factor affecting your premium is your vehicle’s year, make and model. Some vehicles withstand collisions better than others. Vehicle characteristics (such as engine size), passenger protection features (such as air bags) and repair costs affect your premiums.

Cars, light trucks and vans

We use the Canadian Loss Experience Automobile Rating (CLEAR) system, developed by the Vehicle Information Centre of Canada (VICC), to group cars, light trucks and vans. The VICC collects Canada-wide information about vehicles involved in accidents and the cost of claims from these accidents. Cars and vans with similar claim costs and claim risks go into the same rating groups. In all, there are 41 rating groups for cars and light trucks – the higher the rating group, the higher the premium.

CLEAR also gives more favourable ratings to vehicles with factory-installed anti-theft devices that meet the Canadian Theft Deterrent Standard. To meet federal law, any vehicle manufactured after September 1, 2007 must have an approved electronic immobilizer to be sold in or imported into Canada. If you own any 2008 or newer model vehicle, we discount your premium automatically.

Under the CLEAR rating system, a lower value (or older) car may be rated similarly to a higher-value (or newer) car. Here’s why: the lower value car may have fewer safety features and loss-prevention features. Therefore, it may have a poorer claim record than a car that’s worth more.

CLEAR matches your rate with your vehicle’s risk – which changes over time. Vehicles that are less safe and more expensive to fix, cost more to insure. On the other hand, vehicles that are safer and cheaper to fix cost less to insure.

To ensure your premium is correct, we need to identify your vehicle accurately. We do so using the Vehicle Identification Number (VIN) for your vehicle, sometimes called the serial number.

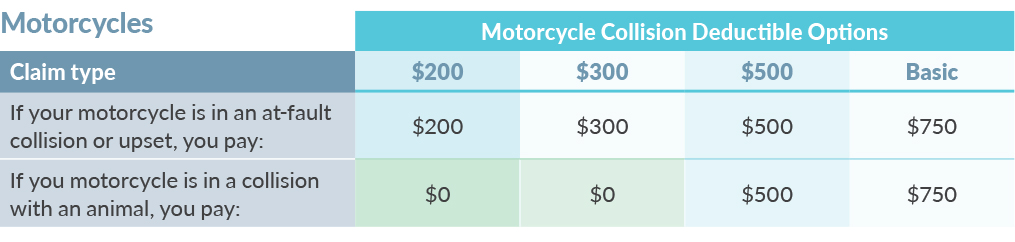

Motorcycles

We rank the risk of motorcycles based on engine size and declared value. Motorcycles are also categorized by type. The categories are: sport, touring, sport touring, motorscooter and other. Premiums for sport bikes are higher than other categories because they have a higher claims risk.

As with other vehicles, motorcycle coverage is year round. However, unlike premiums for cars and trucks, motorcycle premiums are priced over the typical riding season from May 1 to September 30. That means you don’t need to pay your premiums until May 1, and you only pay during the riding season, even though your coverage stays in force all year (unless it expires).

Mopeds

You must meet special requirements to register and insure in the “moped” category.

A moped must:

- have wheels with a diameter of 250 mm (10 inches) or larger

- have a maximum speed of 50 km/h or less

- have an engine displacement of 50 cc or less

- not carry passengers

- not operate on a provincial trunk highway if the speed limit is more than 80 km/hr unless crossing at an intersection in the most direct route

Mopeds can have two tandem wheels or three wheels. It can be driven by pedals, a motor, or both. A motorscooter can also be a moped if it meets the special requirements for the moped category. To ensure your motorscooter is insured properly, ask your Autopac agent.

Motor homes, heavy trucks and buses

We set rates for motor homes based on their declared value. Declaring the value of your motor home means we set the premium based on how much you tell us your motor home is worth. For heavy trucks, we use the model, year and gross vehicle weight. For buses, the rate depends on the declared value and the number of passengers it can seat.

In all cases, declared values include provincial sales tax and GST.

Trailers

This category includes utility, house, cabin or tent trailers used for pleasure, business, u-drive or farm purposes. You must declare the value of your trailer when you register it. A trailer vehicle type includes a body style for cabin or house trailers, which includes (but is not limited to) travel trailers and fifth wheels. Trailers fall into two value categories:

- trailers with a declared value of $2,500 or less

- trailers with a declared value of $2,501 or more

To be eligible for Autopac coverage, a trailer must be mobile and capable of being towed out by the owner within 24 hours without significant modification or cost. Trailers that have been converted into a seasonal or permanent residence or structure are not eligible for Autopac coverage. Conversions can include wheels that are permanently removed, permanent utility connections or permanent add-on decking, skirting or blocking. However, if these modifications are temporary and the trailer is not permanently mounted on a foundation, you may still be eligible for Autopac coverage.

Agricultural equipment (such as a farm trailer) doesn’t need licence plates when transporting farm produce and is towed by agricultural equipment (such as a farm tractor). However, it requires plates when a licenced car or truck is towing it. Autopac options are available for trailers with a value of more than $70,000.

The Drivers and Vehicles Act does not allow the registration of trailers that exceed 2.6 m (102 inches) in width, 12.5 m (41 feet) in length, or 4.15 m (13 feet, 6 inches) in height.

The insurance premium for a trailer valued at $2,500 or less is a flat annual amount, and no refunds are available if you cancel part way through the year. So, we recommend that you renew a trailer policy when you renew your other Autopac so that it’s registered and insured when you need it next.

Remember, the insurance premium stays the same no matter when you renew, and there are no refunds if you cancel.

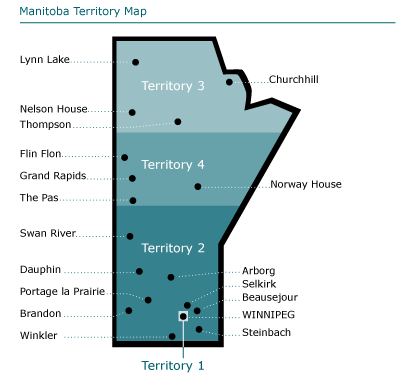

We divide Manitoba into four territories. Your risk of a claim depends, in part, on which territory you live and drive in. Also, accidents may cost more in some parts of Manitoba than others because repairs may be more expensive.

|

Territory 1: |

Winnipeg (including St. Norbert, Headingley, East and West St. Paul) |

|

Territory 2: |

All areas south of the 53rd parallel, except for Territory 1 (includes Brandon, Portage la Prairie, and Dauphin) |

|

Territory 3: |

All areas north of the 55th parallel (includes Thompson, Lynn Lake, and Churchill) |

|

Territory 4: |

The area north of the 53rd parallel and south of the 55th parallel (includes Flin Flon, The Pas and Grand Rapids) |

Commuters

A commuter is a person who lives in Territory 2 and drives into Territory 1 (Winnipeg) to go to or from (or part way to or from) school or work. You must insure as a commuter if you live in Territory 2 and drive into Territory 1 to go to school or work, more than four days a month. For example, a student who lives in Territory 2 but travels into Winnipeg twice a week to attend college must insure as a commuter.

When you move

The law says that your vehicle registration and driver’s licence must show your new address no later than 15 days after you move. If you move from one territory to another and don’t notify us, we may refuse your claim. Ask your Autopac agent to complete an address change for you immediately after you move.

Territory map

How you use your vehicle affects your likelihood of having a claim. Therefore, it also affects your premium.

For instance, if you only drive to the grocery store and back, you’re less likely to have a claim than if you drive your car regularly as a courier.

Having the right insurance for how you use your vehicle is very important. With the wrong insurance, you may not be covered. The following vehicle use definitions will help you ensure that you have the correct type of insurance for the way that you use your vehicle.

Pleasure passenger vehicle

A pleasure passenger vehicle can’t be used for any business purposes. It can only be driven to or from – or part way to or from – work or school up to four days in one month, and not more than 1,609 km to or from work or school during an annual registration period. It can be used to drive dependants to and from school, without limits. Students can’t drive a vehicle to school regularly on pleasure use.

All-purpose passenger vehicle

An all-purpose passenger vehicle is used for pleasure driving and for driving to or from – or part way to or from – work or school, or for business purposes [excluding common carrier passenger vehicle (local)].

Common carrier passenger vehicle (local)

A common carrier passenger vehicle (local) is used by a courier or common carrier within a city or municipality, or for any other delivery purposes in connection with a business, trade or occupation, more than four days in one month or more than 1,609 km during an annual registration period.

Farm passenger vehicle

A farm passenger vehicle is one registered by a person who lives on a farm and who farms for not less than 720 cumulative hours in a registration period or is retired from farming. A retired farmer is not one who has quit farming and taken up another primary occupation. A farm passenger vehicle can only be driven to or from – or part way to or from – work or school or used for business purposes, other than farming, up to four days a month and not more than 1,609 km during an annual registration period. It can be used to drive dependent children to and from school, without limits.

Farming all-purpose truck

A farming all-purpose truck is a truck registered and insured by a person whose primary occupation is farming. It can also be a truck owned by a person, corporation or a group of persons who own, rent or lease land for the purpose of one or more of the following operations (which must be for the purpose of sale or marketing of a product) for at least three months or 720 hours a year:

- growing crops or fodder

- raising livestock or poultry

- egg production

- honey production

- raising mink or fox

- milk or cream production

- operating a feed lot on which cattle are kept

A retired farmer, an employee of a farmer, or a person who owns land and leases it to others for the purpose of farming isn’t eligible for the farming/fishing truck insurance rates. Farming truck has three categories based on the truck’s weight.

A fishing all-purpose truck is used primarily for commercial fishing. Fishing truck insurance uses are divided into three categories according to vehicle weight.

Pleasure truck

A pleasure truck has a gross vehicle weight of 4,540 kg or less and can only be used for pleasure driving. A pleasure truck can only be driven to or from – or part way to or from – work or school up to four days a month and not more than 1,609 km a year. It can be used to transport dependants to and from school, without limits. It can’t be used for business purposes.

All-purpose truck

An all-purpose truck has a gross vehicle weight of 4,540 kg or less and is used for one of these purposes:

- To go to or from, or part way to or from, work or school.

- For business use, such as U-drive, but not for more than 1,609 km per year.

- For artisan truck or other truck use, with one of these body styles: chassis mounted camper, crew cab, extended cab, light delivery, light pickup, panel, sport utility, crew cab service truck, extended cab service truck and service truck.

Motor homes

Motor homes are designed and built for driving and permanent living. Specifically, a motor home must have at least one bed and either:

- a stove

- a refrigerator

- a sink and toilet

Any or all of these items, including the bed or beds, must be permanently installed. Motor homes also must have direct access between the driver’s seat and the living quarters.

- A motor home can be insured in one of three categories:

- A motor home in the pleasure category is used for pleasure driving. It can only be driven to or from – or part way to or from – work or school up to four days a month and not more than 1,609 km a year. It cannot be used for any business purpose.

- An all-purpose motor home can be used for pleasure driving, for driving to or from – or part way to or from–work or school and for business purposes.

- Motor homes can also be U-drives.

Motorcycles and mopeds

Motorcycles and mopeds can be insured in one of the following three categories:

- A motorcycle or moped in the pleasure category is used for pleasure driving. It can only be driven to or from – or part way to or from – work or school up to four days a month and not more than 1,609 km a year. It cannot be used for any business purpose.

- An all-purpose motorcycle or moped can be used for pleasure driving, for driving to or from – or part way to or from – work or school and for business purposes.

- Mopeds can also be u-drives.

Trailers

A trailer is a vehicle that is not self-propelled but is towed by a motor vehicle. It is designed for carrying goods. It includes a farm trailer, but does not include agricultural equipment. It must be mobile and capable of being towed on its own wheels by a motor vehicle. In the event of an emergency, a trailer must be able to be towed out by the owner within 24 hours without significant modification or cost.

A trailer vehicle type includes a body style for cabin or house trailers, which includes (but is not limited to) travel trailers and fifth wheels.